Optimism Under Pressure

Published July 9, 2026

In our last letter, titled “Looking Through the Noise,” we urged clients to do exactly that during a frightening quarter: to separate the short-term shocks dominating the headlines from the durable fundamentals that historically have shaped long-term returns. The geopolitical shock that drove the S&P 500 Index down -4.3% in the first quarter proved to be precisely what we argued it was: a shock to prices, not a reset of earnings power. Over the past quarter, markets have recovered all their losses and gone on to new highs. In fact, the quarter shaped up to be the best for the S&P 500 since 2020, rising 15.2%. The fundamentals we pointed to in April – healthy corporate balance sheets, credit conditions that were not deteriorating, and forward earnings at all-time highs – did not merely hold; in many places they strengthened.

And yet the quarter introduced a subtler and, in some ways, more interesting tension. The very forces powering this market – above all, artificial intelligence – are now drawing the political, regulatory, and public scrutiny that genuinely transformative industries inevitably attract. Inflation has reaccelerated on the back of both the artificial intelligence infrastructure build as well as the war in Iran and energy price shocks. The Federal Reserve has a new and, so far, surprisingly hawkish Chair. The national debt has quietly crossed a historic threshold (>100% of GDP). The central question shaping our thinking today is no longer simply whether to look through the noise; it is whether the remarkable strength of corporate fundamentals can continue to outrun the constraints – geopolitical, monetary, regulatory, and valuation-related – now building around them. This is the balance we have come to think of as optimism under pressure.

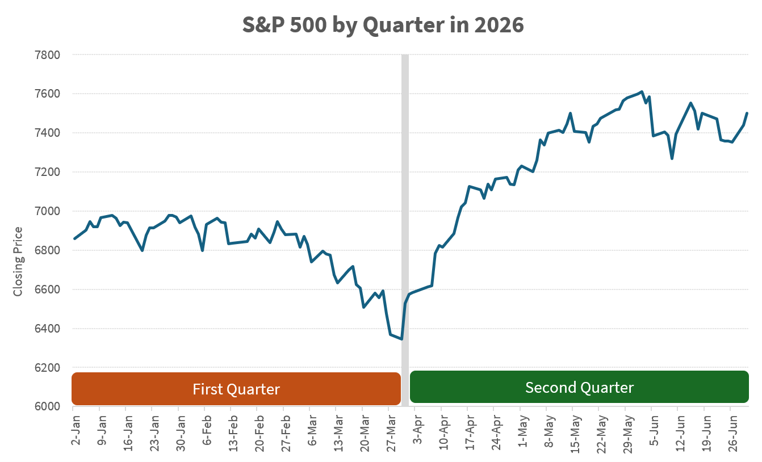

The market’s round trip this quarter was historic. From its first quarter peak, the S&P 500 fell 9.1% before reversing course entirely; at one stretch the index returned roughly 10% in just ten trading days – a move, according to Bloomberg, in the top 99.7% of all ten-day periods in the history of the index. Investors were reminded, abruptly, that earnings were good and getting better. But beneath that exuberance lies a striking divergence: the University of Michigan’s Consumer Sentiment survey fell to its lowest level in the history of the series, which dates to 1952. Wall Street and Main Street have rarely told such different stories at the same moment. This “K-shaped” reality – financial markets and asset owners thriving, while household sentiment sours under the weight of higher gasoline and grocery prices – is, in our view, one of the defining features of this moment, and one with real political consequences for future elections.

Source:YCharts as of 6/30/2026

Geopolitics: The Shock Begins to Pass

In April, we wrote that the greatest risk from the Iran conflict was not the conflict itself but how long it lasted and how broadly it spread. For much of the quarter, duration was precisely the problem. After an initial cease-fire, the conflict settled into an uneasy stalemate, with neither escalation nor resolution appearing imminent. The domestic political costs accumulated: national-average gasoline prices topped $4.50 per gallon, the administration moved to suspend the federal gas tax, and reports emerged of U.S. munitions stockpiles running low. Throughout, our working framework held up well – that President Trump required a credible, clearly articulated victory to bring the conflict to a close, whether through a durable agreement halting Iran’s nuclear ambitions or the removal of enriched uranium.

As we write this letter, an already fraying Memorandum of Understanding has been thrown into further doubt after President Trump declared the ceasefire “over” following a fresh exchange of strikes between the US and Iran. We cautioned in April that Mr. Trump’s instinct under pressure has often been to double down, and that an expansion of the conflict would have changed our calculus; with strikes now being traded and talks reduced to what he calls a “waste of time,” that risk appears to be back in play. Politics aside, markets have reacted accordingly, with oil prices surging on the news as the prospect of a freely-moving Strait of Hormuz recedes for now. We would temper expectations on resolution and timing; even before this latest escalation, energy prices were likely to take time to fully normalize, and the two sides still appear to be a ways apart in negotiations. It remains to be seen whether this proves a rhetorical flare-up that gives way to renewed talks, or a genuine reopening of what had been one of the largest tail risks hanging over the market in April

Inflation and a New Fed: Higher for Longer

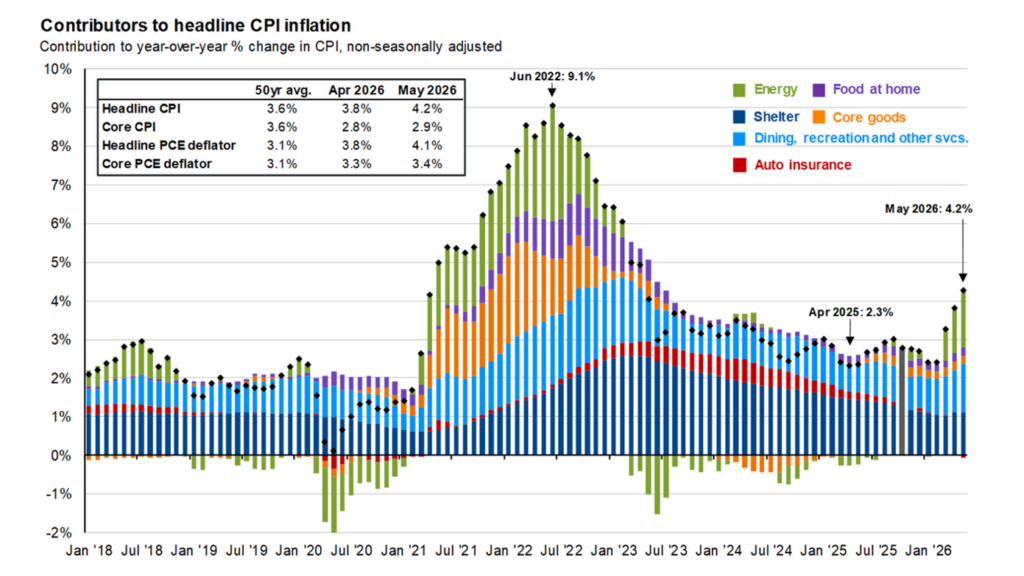

Whether or not geopolitical risk is receding is now an open question – but its economic aftershock is not. The energy spike caused by the closing of the Strait of Hormuz fed directly into prices, and inflation reaccelerated steadily through the quarter: headline CPI rose from 3.3% in March to 3.8% in April and 4.2% in May. This is the most consequential change to the macro backdrop since our last letter, and it arrived just as the Federal Reserve underwent a historic leadership transition.

Source: BLS, FactSet, J.P. Morgan Asset Management.

Jerome Powell’s final meeting as Chair was an eventful one, drawing four dissents – the most since 1992 – as the committee wrestled with reaccelerating inflation. He has been succeeded by Kevin Warsh, who arrived with a reputation as an advocate for lower rates, and whom President Trump has openly hoped would deliver cuts. The data, however, have not cooperated. At Mr. Warsh’s first meeting as Chair, the Fed held rates steady at 3.50%–3.75% and signaled a more neutral-to-hawkish, “higher-for-longer” posture. The shift followed a notably strong labor report (May payrolls rose by 172,000 against expectations of roughly 80,000) alongside that further uptick in inflation. In a rising-price environment an easing bias would have been historically unconventional, and the new Chair appears, at least for now, to be charting an independent course (as a further institutional check, Mr. Powell is expected to remain on the Board through 2028).

For portfolios, the implication is straightforward, and one we positioned for early: we have kept the duration of our bond holdings short, a decision the more restrictive Fed has rewarded.

Artificial Intelligence Frictions Continue

Artificial intelligence remains the most powerful structural force in the market, and our conviction in it as a multi-year source of earnings growth is undiminished. But the character of the AI story changed meaningfully this quarter in two respects that matter a great deal for how this story plays out.

The first is a shift in the bottleneck – and therefore in where the value is accruing. For several years, the narrative has centered on the graphics processing units (GPUs) that do the computing. In our quickly approaching “agentic” world, the constraint is increasingly memory. The analogy making the rounds is apt: if the GPU is an increasingly faster car, memory is the road, and the car can only travel as fast as the road allows. As AI evolves from chatbot to agent – systems that hold larger context, retain individualized memory, and act over longer horizons – the speed of delivering information to the processor matters as much as the processor itself. Anthropic recently unveiled a feature called “Dreaming,” in which an agent reviews its prior sessions overnight and writes itself new memory; as more agents “dream,” those memory needs increase. This is one of many examples of advances that have propelled the high-bandwidth memory supply chain – dominated by South Korea’s SK Hynix and Samsung – to the center of the trade, leading Korean equities to be among the best-performing in the world this quarter. As Nvidia’s Jensen Huang put it, HMB (high-bandwidth memory) “will likely be the largest storage market in the world.”

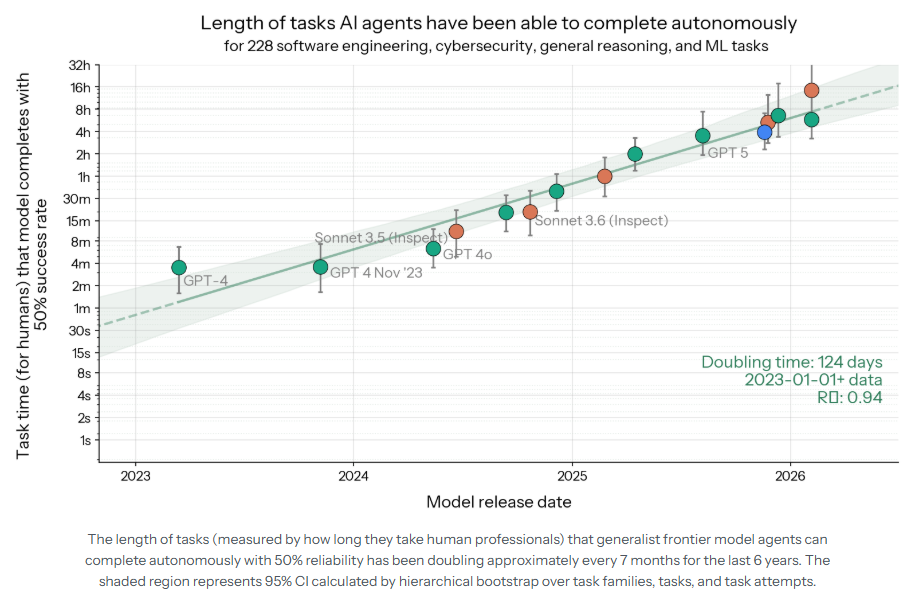

Source: METR, “Measuring AI Ability to Complete Long Tasks”

The second shift is more profound, as a more diverse coalition – spanning economic, security, religious, and political concerns – has begun to push back on the technology. After years of a largely hands-off posture, the federal government issued an export-control directive restricting access by foreign nationals to Fable 5 – the most capable commercially available frontier model at the time – a step that forced Anthropic to disable its most advanced systems for all users for several weeks, unable to verify citizenship. This came after Anthropic’s most powerful model Mythos was initially deemed too capable to release broadly after it uncovered a startling number of security vulnerabilities (including a flaw in widely used software that had gone undetected for 27 years) and was distributed first to “the good guys” through a cybersecurity initiative before any wider availability. The model was so capable of finding cybersecurity flaws that Treasury Secretary Bessent convened an emergency meeting with bank CEOs on the subject. Beyond the executive branch, the state attorney general in Florida has sued OpenAI alleging its product is unsafe, Senator Bernie Sanders introduced the American AI Sovereign Wealth Fund Act which proposes a one-time 50% tax on the largest AI firms, and Pope Leo XIV, in his first encyclical, warned that AI must be “disarmed.” Data-center moratoriums are also becoming a live local political issue across the country, including here in Maine.

We do not read these developments as a reason to abandon the theme, though they do warrant a more measured approach. Transformative technologies attract scrutiny precisely because they are transformative, and history suggests the largest, best-capitalized, most trusted platforms tend to navigate regulation more successfully than smaller competitors, often emerging with wider competitive moats. But the risk profile has changed: the next phase of AI-driven growth will be shaped at least as much by regulation and public acceptance as by raw technological capability. That argues, as we wrote in April, for being committed but selective: getting exposure through companies with the scale, balance sheets, and trust to invest through cycles and to absorb a more demanding regulatory environment.

Froth at the Margins: SpaceX

The enthusiasm around growth and technology has, in places, detached from fundamentals. The clearest illustration this quarter was the IPO of SpaceX – an extraordinary company whose initial offering was priced at roughly 94 times the prior year’s revenue, a valuation so extreme that we have seen analysts using logarithmic scales to chart it against its peers. The offering was, in our reading, a masterclass in manufactured scarcity: a float limited to 5% of the shares, expedited inclusion in major indices to compel passive buying, and an unusual cultivation of retail demand. The stock predictably had an initial surge but has since retreated from those highs. We expect the stock price to be volatile over the next year as restrictions on shares progressively come off. We hold SpaceX in high regard and expect it to succeed over time, but as fiduciaries we have decided to wait for a better price. It is a useful reminder that price and value are not the same thing, and that our job is to be disciplined about the difference even when the crowd is not.

Staying Disciplined

A year that began with war and a market correction has, at its midpoint, delivered new highs, the glimmer of peace, and a fresh set of questions. The optimism in markets is real and, importantly, it is earnings-backed – this is not 1999. But it is optimism under pressure: pressed by a more restrictive Fed, by reaccelerating inflation, by a growing public and political backlash against the very technology driving returns, and by valuations that in places have run ahead of reason. The defining question for the quarters ahead is whether resilient fundamentals can continue to outrun those constraints, or whether one side of the equation eventually forces a repricing.

We are also watching the political backdrop closely. The midterm elections are now roughly four months away, and the K-shaped economy – record markets alongside the weakest consumer sentiment on record – is precisely the kind of dynamic that shapes elections and, in turn, policy. The President’s willingness to seek an off-ramp in Iran, even briefly, suggested that he, too, feels the pressure – though today’s reversal is a reminder of just how quickly that calculus can flip. The midterm results will matter a great deal for Trump’s direction of travel over the remainder of his presidency. A Democratic House could mean legislative gridlock, a Democratic Senate could stall confirmations, and either outcome would reshape the market’s read on what’s achievable in the back half of this term.

Our response to all of this is not reinvention but discipline. We are making incremental adjustments – rebalancing toward targets, trimming froth, keeping duration short, and sharpening our positioning in the parts of the AI supply chain we find most compelling – rather than wholesale changes, consistent with our long-held belief that durable results come from thoughtful allocation rather than reaction to the day’s narrative. As we wrote three months ago, our focus remains on great businesses with durable earnings power over the next three to five years – not on the next three to five headlines, however loud they have become lately.

The Spinnaker Trust Investment Team