Staying the Course – Third Quarter 2025

Published October 8, 2025

Staying the Course – Third Quarter 2025

In the third quarter, the combination of a resilient US economy and massive investments in all things related to artificial intelligence, supported by fiscal easing and, more recently, monetary easing, continued to outweigh policy-related uncertainties. While various labor indicators are flashing warning signs that the economy may be slowing (a logical reaction to the uncertainty created by recent tariff policies),earnings, driven by the largest technology platform companies, for the second quarter were outstanding. Against this backdrop, the S&P 500 charged ahead, finishing the quarter up 8.1%, contributing to year-to-date gains through quarter-end of 14.8%. The ten-year Treasury finished the quarter at 4.15%, relatively unmoved from the end of last quarter, where it was 4.2%, despite the Federal Reserve cutting rates by 25bps (or ¼ of 1%).

Federal Reserve Policy: A Balancing Act

With tariff policy volatility easing and the Big Beautiful Bill passed into law in early July, the market’s attention shifted to Federal Reserve policy. Over the course of the year, President Trump has greatly increased pressure on the Federal Reserve to reduce rates. Trump has continuously criticized Jerome Powell, the chair of the committee, and most recently attempted to fire a Fed Governor, Lisa Cook, for alleged mortgage fraud. In response, the Federal Reserve Board appears to have kept a firm hand on the tiller and appears so far to be reacting more to data than external pressure. All eyes were on the Fed in September when they approved their first rate cut in nine months and signaled more may follow this year – a notable pivot from their earlier stance of holding rates steady due to inflation concerns tied to tariffs. While input costs from tariffs have risen, so far, the consumer impact remains limited, and there appears to be growing confidence that tariffs may produce a one-time price shock (perhaps spread over time) but are unlikely to trigger an inflationary spiral.

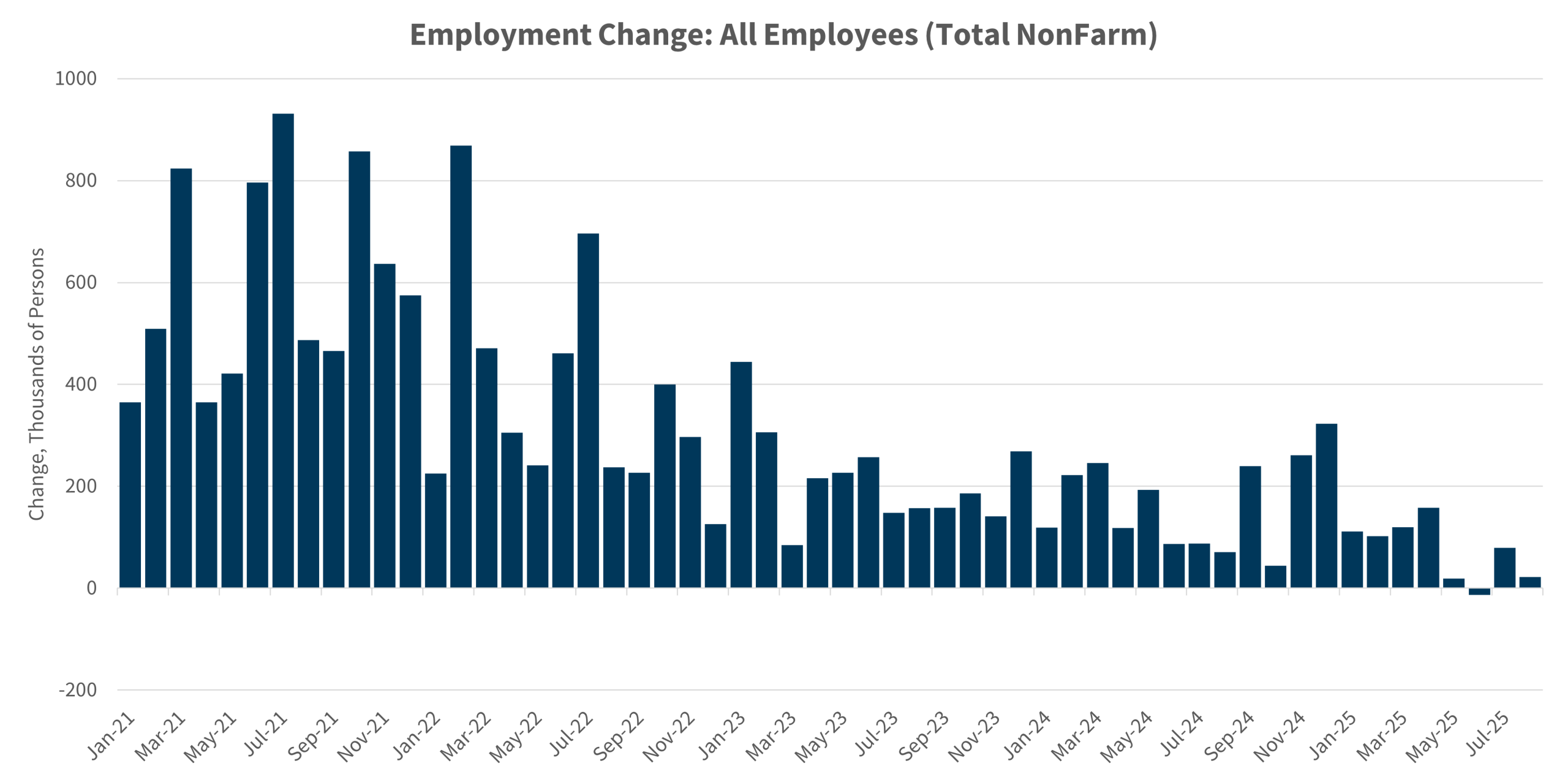

In August, the Fed turned its focus to the labor market after revised data revealed a sharp slowdown in job growth. The May and June reports were revised down by a combined 258,000 jobs, prompting political backlash, including President Trump’s call to dismiss the Bureau of Labor Statistics (BLS) chief. We believe these revisions (May down to 19,000 from 144,000 and June to 14,000 from 147,000) were determinative as the Fed chose to address the risk of a slowing economy rather than continue to protect against the potential for returned inflation.

Source: U.S. Bureau of Labor Statistics via FRED (St. Louis Fed)

The Supreme Court is currently reviewing a case concerning the attempted removal of Federal Reserve Governor Lisa Cook, which could have significant implications for the balance of power between the executive branch and independent agencies. At the heart of the case is the interpretation of the Federal Reserve Act’s “for cause” provision, which limits presidential authority to dismiss Fed officials. A ruling that broadens this authority could materially impact the Fed’s institutional independence.

There are of course different opinions on the extent of presidential powers, as well as the protections that should be afforded independent agencies, but from a market perspective there are good reasons for the Federal Reserve to be seen as independent. Easy monetary policy is in the interest of every president, as it can be used to increase economic velocity in the short-term. This economic velocity, however, can quickly lead to overheating and an inflationary spiral that is difficult to stop without large, painful interventions. An independent Fed can be better positioned to make policy decisions based on economic fundamentals rather than political considerations, contributing to more stable and predictable outcomes. As it stands currently, we see the Federal Reserve acting prudently, responding to labor market weakness while not acting too fast as they wait and see how the effects of tariffs bleed into consumer prices.

Legislative Update: Tax Cuts and Innovation Incentives

The One Big Beautiful Bill Act was signed into law on July 4th. The central thrust of the bill was to extend the 2017 tax cuts, which were scheduled to expire. This is the biggest ticket item in terms of cost but will provide a boost to companies and consumers as lower tax rates remain in place. Importantly, the bill also makes permanent historically high estate, gift and generation-skipping transfer (GST) tax exemptions that otherwise would have been reduced to approximately $7,140,000 at the end of this year. The new legislation locks in and increases these exemptions to $15 million per individual beginning on January 1, 2026 (with inflation adjustments beginning on January 1, 2027). Also included in the bill were bigger income tax deductions for state and local taxes, known as SALT, which will last through 2028. Fulfilling one of Trump’s campaign promises, tips and overtime wages will no longer be taxed (capped at $25k). The potentially biggest effects from a market perspective were immediate deductions for research and development expenditures and accelerated depreciation for capital expenditures, leading to even larger AI-related capex for the large tech companies.

Artificial Intelligence and Market Leadership

Markets appear to be looking past near-term risks, pricing in easier monetary policy and continued innovation-led growth. Earnings season surprised to the upside, with aggregate year-over-year earnings growth at 12% vs. 5% expected. Overall sentiment has improved, with “recession” mentions on last quarter earnings calls down 84%. However, growth was concentrated: two-thirds came from the Communication Services and Technology sectors. The “Magnificent 7” continue to dominate, with projected 2025 earnings growth of 21% year-over-year vs. 7% for the rest of the S&P 500. AI demand remains strong, but is constrained by computing capacity, driving massive capex: $315B projected in 2025 by Alphabet, Amazon, Meta, and Microsoft, or ~60% of their operating cash flow.

OpenAI’s CEO Sam Altman declared in June, “We are past the event horizon; the takeoff has started. Humanity is close to building digital superintelligence…” Artificial intelligence has become the lynchpin for growth in the tech industry as massive capex and ferocious AI talent wars have dominated conversations. The primary investor question remains: when will these substantial investments begin generating revenue commensurate with their scale? We remain bullish on the long-term potential of AI, but we are increasingly mindful of valuation and concentration risk as well as the larger societal risks this type of technology may bring.

Spinnaker Portfolio Positioning and Outlook

For clients of Spinnaker Trust, the last quarter was highly successful as we were exposed to many of the themes dominating the markets and have earned high absolute returns for clients. In our ETF models we have been correctly overweight the Technology sector and, in particular, semiconductor companies that are building the infrastructure needed for AI to bear fruit. Our allocation to small cap stocks contributed slightly to performance (up 9.2% over the quarter), as the potential for lower rates is seen as a boost to these small companies which are generally more sensitive to interest rates due to their higher reliance on debt. Allocations to uranium (tied to renewed interest in nuclear power) and gold have been strong contributors to our alternatives allocation, and our international allocation, which helped drive high absolute performance early in the year, has kept up with the strong US markets.

Looking forward, we remain fully invested within our equity portfolios as both monetary and fiscal policies have turned accommodative, and the AI wave continues to unfold in what we believe are still early innings. However, we are keeping a close eye on the risks: the concentration of returns in a small slice of companies, labor market weakness, fiscal imbalance, and the potential for the return of inflation as tariffs continue to impact consumer prices. Recent events in Ukraine and in Europe also bear mention. President Trump appears to be recognizing Vladimir Putin as the intractable foe that others have been calling out for years. The war appears to be entering a new phase where the US and Europe may more fully support Ukraine and try to make the war less sustainable for Russia. There are obviously numerous risks that accompany this shift. Meanwhile, China seeks to exploit the situation for its advantage, linking in the complex negotiations over the future trade relationship with the US.

The balance we are trying to strike is to maintain appropriate and prudent diversification at a time of heightened risks across a wide range of axes – while maintaining adequate exposure to the technology revolution that continues to unfold around us. Markets are not perfect; they frequently overshoot in both directions. The US equity market is expensive by any reasonable measure, but the prices of the leading technology companies are supported by competitive moats, fortress balance sheets and tangible opportunities for continued growth. We remain vigilant looking for threats to those moats or opportunities for growth. As we travel around the world, it is striking to see the degree to which US (or in some cases Chinese) technology has been adopted into everyday life. Apple and Google dominate the operating systems for billions of phones worldwide, all running thousands of software applications that are making everyday life more productive, connected and enjoyable. This is the single most important economic event of the past quarter century, and artificial intelligence offers the potential for a whole further round of adoption and gradual monetization. We want our clients to participate in that growth and transformation while trying to sidestep the detours or excesses that inevitably accompany enormous technological innovation.