Looking Through the Noise

Published April 8, 2026

The first quarter of 2026 was a reminder that uncertainty rarely arrives one variable at a time and that these variables are often interconnected in uncomfortable ways. Geopolitical escalation, continued rapid technological change, and structural imbalances in the relatively new private credit markets competed for attention in the first quarter, each a risk and each connected in a narrative link. In the short term, the escalating war in the Middle East became the dominant driver of markets, and the S&P 500 Index finished the quarter down -4.3%. With the price of oil, and therefore gasoline, surging, inflation concerns reemerged, and the ten-year United States Treasury bond finished the quarter at a yield of 4.3%.

We wrote in January that the only certainty is change – but not all changes are consequential. Long‑term outcomes are most often shaped by shifts in durable fundamentals, not by the short‑term noise of market shocks. Making the distinction represents the challenge of this moment.

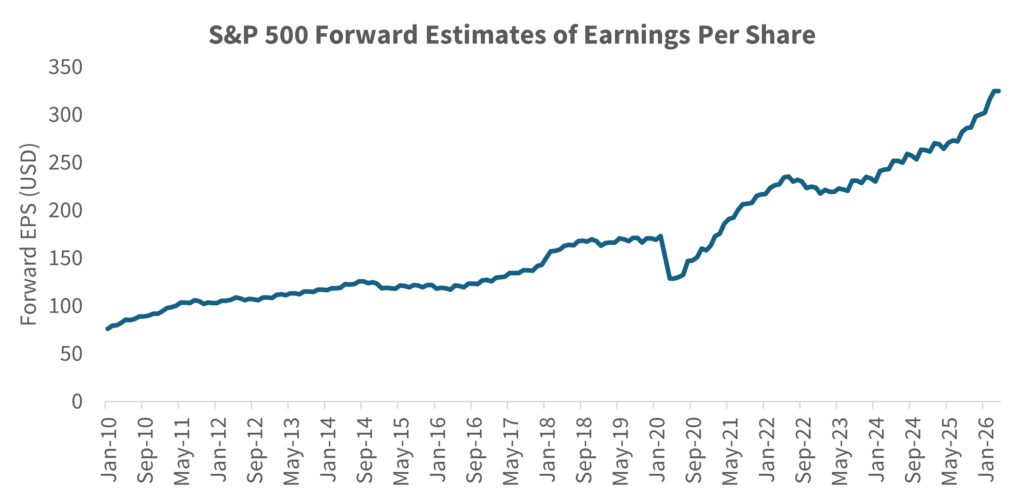

Despite a dramatic news cycle, our central views on the durable fundamentals are unchanged. Corporate balance sheets in the US are healthy, credit conditions are not deteriorating in a way that suggests systemic stress, and forward S&P 500 earnings estimates are still at all-time highs. Our task is not to predict the next headline, but to distinguish short-term volatility (i.e. Iranian conflict at least as advertised) from structural change (i.e. AI acceleration) and position portfolios accordingly.

Source: Bloomberg

This quarter, three themes dominated our thinking: geopolitics – particularly the conflict with Iran; artificial intelligence and its implications for software and productivity; and private credit concerns created by those perceived threats to software.

Geopolitics: A Serious Shock, but Not a Structural One – Yet

This quarter delivered an unusual concentration of geopolitical shocks, led by the United States’ military action in Iran but extending to events as disparate as the capture of Nicolás Maduro in Venezuela and the attempted seizure of Greenland from our allies. Relative to the Iran conflict, markets reacted predictably compared to past Middle Eastern events: energy prices spiked (brent crude oil has reached close to $120 per barrel), volatility increased, and investors quickly focused on worst‑case scenarios, particularly around a prolonged disruption of energy flows through the Strait of Hormuz, a critical chokepoint for roughly one-fifth of global oil and gas flows.

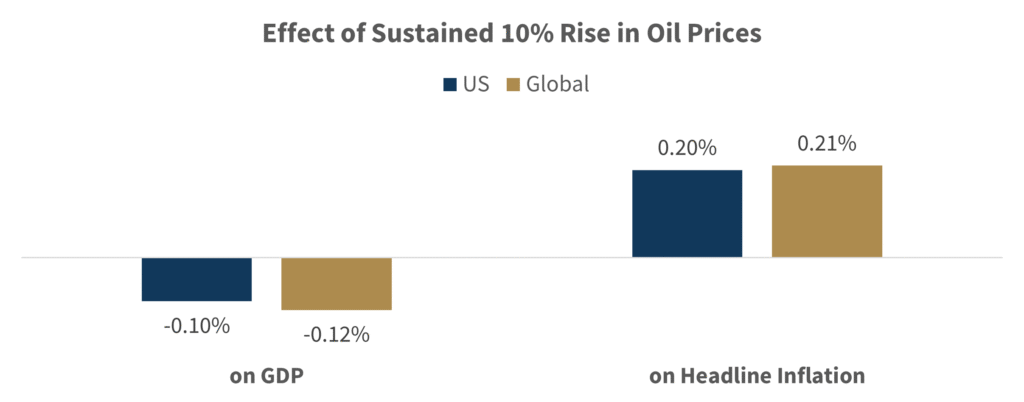

From a market perspective, the key risk was and remains the duration of the conflict: while baseline expectations assumed contained economic impact, a sustained disruption to energy supply could pose meaningful downside risks to global growth, margins, and risk assets more broadly. In other words, the greatest risk is not the conflict itself, but how long it lasts and how broadly it spreads. To date, while energy prices have moved higher, broader economic indicators do not yet suggest a sharp deterioration in demand, credit conditions, or corporate investment plans. Analysts have estimated that the effect of a sustained 10% rise in oil prices to be -0.12% of GDP and +0.21% increase in headline inflation globally.

Source: Goldman Sachs Global Investment Research and Goldman Sachs Asset Management as of March 5, 2026. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation.

History also offers a useful perspective. Geopolitical shocks often feel existential in real time, yet their long-term market impact is typically far less than initially feared unless they fundamentally impair capital formation, labor markets, or the global financial system. Looking at past conflicts, the S&P 500 historically falls 5-7% in the first 10 days of a new conflict, flattens by day 35, and gains 8-10% within 12 months (Source: RBC). Accordingly, we have not materially repositioned portfolios around the Iran conflict, viewing energy-driven volatility as a shock to prices rather than a reset of earnings power.

Source: Bloomberg. Goldman Sachs Global Investment Research and Goldman Sachs Asset Management

AI, Software, and the Market’s Fear of Disruption

If geopolitics dominated headlines, artificial intelligence dominated investor psychology. Over the quarter, markets increasingly grappled with the implications of agentic AI (systems capable of performing complex, multi-step tasks with minimal human supervision) on software. These concerns gained traction following Anthropic’s release of Claude Code 2.0, an advanced coding agent capable of understanding and modifying massive codebases through an agentic loop of context gathering, action, and verification. Anthropic has been explicit that AI now writes the majority of its code internally, shifting engineers’ roles from writing software to supervising and guiding AI output. This evolution, alongside the emergence of popular open‑source agents such as OpenClaw (which grants AI full-system access to autonomously perform real‑world tasks for individuals) has intensified fears that AI could rapidly commoditize large portions of enterprise software.

These concerns are legitimate, but we believe the market is overly conflating disruption with destruction. Technological revolutions rarely eliminate entire categories of value creation; instead, they redistribute value. Some software will become redundant – this is inevitable and healthy. But software gives us more than lines of code, it provides tools that efficiently solve problems with built-in trust, security and maintenance that are often done better at scale. These attributes are not easily replaced by raw intelligence alone and instead can be critical and efficient tools for agents to use to accomplish their objectives. In many cases, we expect AI agents will depend on software platforms rather than displace them, using them as systems of record, orchestration layers, and secure interfaces. We also believe that any collapse in certain software categories would represent an offsetting gain for AI and its enablers. As 3Fourteen Research succinctly put it, “the more pessimistic your software assumptions, the more optimistic your AI assumptions.” As with prior technology cycles, the winners will be those platforms that integrate AI most effectively into their ecosystems, enhancing productivity while maintaining trust and reliability at scale.

This premise is why we remain committed to technology exposure, while being increasingly selective. The benefits of AI will not accrue evenly, and value creation will continue to concentrate among companies with scale, data, distribution, and balance sheets strong enough to invest through cycles. Semiconductor exposure, for instance, becomes increasingly important in an agentic age, as these agents require smarter, faster and more chips to support at scale. Over our longer-term time horizon, we continue to believe technology, and especially semiconductor stocks, will be one of the most attractive sources of earnings growth in the market – even if the path is volatile.

Private Credit and Liquidity: More Noise Than Signal So Far

The final theme of the quarter was growing retail investor concern around private credit (where investors lend money directly to companies instead of that company borrowing from a bank or issuing bonds in the public market). A large portion of these loans have been made to software companies, raising concerns that if software businesses are disrupted by new artificial intelligence tools, the private credit funds lending to them could also be impacted. This has led to investors attempting to pull capital from newly launched semi-liquid vehicles.

While plausible, this scenario assumes a speed and severity of deterioration that we simply do not see in the data today. Of the software companies that we follow, we have not seen any irregular churn with their customers, and many were still able to raise prices over the last few quarters. We have also not seen a meaningful deterioration in non‑accruals across the private credit portfolios we monitor. A non‑accrual loan is a loan where the borrower has stopped making expected payments, so the lender stops counting the interest as income, an important indicator of credit stress. In the most transparent segment of the market, Cliffwater’s data (which tracks nearly 20,000 loans across publicly traded, non-traded and private BDC portfolios) shows that non‑accrual rates remain low and below 10-year historical averages.

The fundamental challenge relating to private credit is that an inherently illiquid product was placed into appropriate, limited liquidity structures, but these were then sold to retail investors, many of whom did not have the long-term perspective required to invest in illiquid assets. Faced with the mere potential for a more challenging environment, these investors attempted to flee, creating the appearance of a crisis. The long-term performance of the loans in a portfolio will ultimately determine the performance of these vehicles, unless their managers panic and attempt to meet all liquidity demands through the immediate sale of portfolio assets. We believe the most experienced managers will weather this period and emerge stronger. Here again, the market appears focused on near-term uncertainty and a retail investor panic rather than data or long-term economics.

From a longer-term perspective, private credit exists because it fills a structural gap left by regulated banks that abandoned the market after the Great Financial Crisis in 2009 due to increased bank regulation. That gap has not closed; if anything, it has widened. Periods of stress tend to favor scaled, disciplined managers with access to capital and the ability to deploy opportunistically – precisely the types of managers and businesses we favor. Over a multi-year horizon, we continue to view financial stocks – particularly those tied to asset management, insurance, and credit intermediation – as well positioned.

Staying Anchored to What Matters

As we look ahead, this past quarter’s headlines have done little to change our core views. Most broadly we haven’t yet seen material credit deterioration or a collapse in corporate fundamentals that would indicate a coming recession – in fact, credit spreads are tight and forecast earnings in the US are at highs. We also do not believe short-term geopolitical shocks, as Trump has described the current conflict with Iran, should dictate long-term portfolio strategy without a corresponding change to long-term fundamentals.

We are, however, closely monitoring the political challenges that are beginning to mount for President Trump. Trump’s overall approval rating was 45%-47% in early January, but it declined to 39%-42% by late March. The largest factor is almost certainly the war in Iran, where, despite impressive military operations by the US and Israel, including eliminating key Iranian leaders, the Iranian regime has remained operational and has demonstrated the ability to effectively close the Strait of Hormuz. Allies have declined to join the war, and oil and gas prices have been highly volatile.

Trump has also faced additional domestic challenges in the first quarter. The bulk of his tariffs were overturned by the Supreme Court; two US citizen deaths in Minneapolis were broadly seen as the result of improper and possibly illegal action by ICE; the Epstein files continue to receive extensive press coverage; and, most recently, Congressional Republicans refused to follow the President as they seek to fund the Department of Homeland Security.

The mid-term elections are now six months away, and Trump recognizes that a Democratic majority in the House or Senate will result in his final two years being marked by gridlock from a legislative perspective with multiple investigations of him, his family and his administration. We point out Trump’s increasing political vulnerability primarily because his response to adversity has often been to double down, which in this case could mean pushing further in the Iranian conflict in hopes of achieving regime change – or at a minimum, removal of uranium. We have said a number of times that Trump has an enormous appetite for risk, and we must acknowledge that the pressure has been building, so we cannot rule out the possibility that he will choose to expand military operations in Iran – a step that would change our calculus on the temporary nature of the current challenges for equity markets. While the recently announced cease-fire offers an important escape valve for some of the built-up pressure, the underlying issues remain largely unresolved, negotiations are only beginning, and in our view the risk of additional setbacks – and short-term market volatility – remains high until Trump can find a credible victory in this conflict.

Our tactical positioning continues to emphasize technology, financials, and healthcare sectors that we believe are best positioned to compound earnings years into the future. Healthcare, not discussed in this letter, remains underappreciated as a defensive growth sector, benefiting from demographic tailwinds, innovation, and relatively insulated demand.

The next several weeks are likely to be determinative in terms of the direction of the Iranian conflict. We expect that markets will continue to test everyone’s patience, including our own, but history shows that markets reward discipline over reaction. Our focus remains on great businesses with durable earnings power over the next 3–5 years, not on reacting to the next 3–5 headlines.