Published November 6, 2025

Executive Summary

Equity markets have continued their upward trajectory in 2025, supported by monetary easing, fiscal stimulus, and a surge in AI-driven innovation. Since the launch of ChatGPT in late 2022, AI-related companies have dominated market performance, contributing roughly 75% of S&P 500 returns and 80% of earnings growth. This concentration has sparked debate over whether we are in an AI bubble, particularly as valuations in some areas resemble those seen during the dot-com era. For example, over 30% of the S&P 500 trades above 10x sales, and private market valuations—such as OpenAI’s recent $500B raise on $13B in revenue—underscore investor optimism. Concerns have also emerged around “circular revenue” arrangements, such as Nvidia’s $100B investment in OpenAI, which plans to use those funds to purchase Nvidia chips.

While pockets of excess are evident, today’s environment differs meaningfully from 2000. AI’s economics are rooted in scalable compute infrastructure and neural scaling laws, which predictably link performance improvements to increased investment in data, model size, and compute power. This dynamic creates network effects and positions AI as a foundational technology with a vast addressable market—potentially extending beyond human labor productivity. Moreover, leading firms exhibit stronger fundamentals than their dot-com predecessors, with higher margins, returns on equity, and robust balance sheets. Risks remain: if revenue growth slows or innovation stalls, valuations could compress. However, given accelerating adoption and the potential for transformative applications, we believe the long-term opportunity in AI remains compelling, even if near-term volatility persists.

The markets continue to grind higher so far in 2025 despite headlines full of worry. While tariff concerns remain, they are currently being outweighed by both monetary and fiscal stimulus with the market still being driven by AI-related innovation and investment. With the Big Beautiful Bill behind us, and the Federal Reserve starting a rate-lowering cycle, the wall of worry has shifted to the core of today’s market strength with investors asking: are we in an AI bubble? This is an existential question for the current market since the ChatGPT launch in November of 2022, some analysis has shown that AI-related stocks have accounted for 75% of S&P 500 return, 80% of earnings growth and 90% of capital spending. While these concerns have been around for a while, they were officially kicked into the public consciousness in August when OpenAI CEO Sam Altman said in an interview:

Are we in a phase where investors as a whole are overexcited about AI? My opinion is yes.”

This meme of an AI bubble has accelerated lately with conversations shifting to the quality of earnings for some of the biggest AI companies, especially as related to “circular revenue.” The poster child of this criticism has centered on a recent deal where Nvidia (an AI chip maker) agreed to invest $100B in OpenAI, with OpenAI planning to use that $100B to buy Nvidia chips, which Nvidia will book as revenue – leading to questions from investors on the quality of that revenue. The market has noticed several of these types of arrangements in the past few weeks, transactions which seem on their surface to have good reasons, but have historically raised eyebrows. In the case of OpenAI and Nvidia, there are clear reasons why this transaction makes sense for both sides, as there remains massive demand for Nvidia chips and OpenAI doesn’t have any obligations to use that capital to buy Nvidia chips (and in fact has expanded its supply chain to include their own chips and has since made partnerships with several other chip makers), but it does raise questions of whether the purchases would have been made if not for the capital investment.

These bubble conversations and comparisons to the dotcom era are also not without merit. Over 30% of the S&P 500 trades above 10x sales, with 13% above 20x—levels reminiscent of 2000. Palantir Technologies, as an example, is trading at an eye-watering 89x Price to Sales (CY25E), prompting our memories of this quote from 2002:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking? “

– Scott McNealy, CEO of Sun Microsystems in 2002, discussing its share price in 2000.

As an example of these lofty valuations, in OpenAI’s latest round that included the capital from Nvidia, they raised at a $500B valuation, despite only $13B in revenue and cash losses expected to exceed $8B this year.

While we are certainly seeing pockets of excess (particularly in the private markets) and these questions do keep us up at night, we think that the situation today is potentially quite different from the dotcom bubble in a number of ways.

The first is found in the nature of the technology itself. In the dotcom era, the utility of computing hardware (like a PC or router) was largely individual and localized. Each additional device had diminishing marginal returns because the value was tied to a single user’s access or a single node’s capacity. The network effects were more about connecting users than scaling compute.

In contrast, today’s AI era is characterized by scalable, centralized compute where each additional GPU or specialized chip (like TPUs) contributes to a shared intelligence infrastructure. This infrastructure supports both training (more compute enables larger, more capable models) and inference (more chips allow for broader and faster deployment of those models). This creates increasing returns to scale as each additional unit of compute can improve model performance and serve more users, often simultaneously. We have moved from an era of single-node utility in the dotcom era to an era of scalable intelligence infrastructure, which shifts the total addressable market of the technology from penetration of each home and office to the total addressable market of current paid compensation of human intelligence and potentially beyond.

The huge amounts of capex from the large technology companies are also rooted in AI scaling laws. Neural scaling laws were formalized in a 2020 paper by OpenAI researchers and showed that the performance of AI models improves smoothly and predictably as you scale model size (number of parameters), dataset size and importantly: compute power (training time, hardware resources). There is also a pretraining scaling law, relating specifically to the training phase, that states that larger models trained on more data with more compute tend to perform better, a law foundational to the development of large language models. These scaling laws support the belief that scaling compute is the fastest path to a more capable AI, especially towards the golden goose of artificial general intelligence (AGI) that can self-improve. This buildout represents a self-reinforcing network effect, where the larger superclusters make more capable models, can serve more customers and importantly also attract the best talent (who want to work on the largest superclusters).

Technology aside, the companies today also have significantly stronger financial fundamentals than their counterparts in 2000. If we take the tech bubble leaders from 2000 (Microsoft, Cisco, Intel, Oracle, IBM, Lucent and Nortel Networks) and compare their fundamentals to that of the Magnificent 7 in 2025 (Microsoft, Apple, Nvidia, Amazon, Alphabet, Meta and Tesla), Mag 7 fundamentals dwarf 2000 tech leaders: ROE 46% vs 28%, margins 29% vs 16%, and stronger balance sheets.

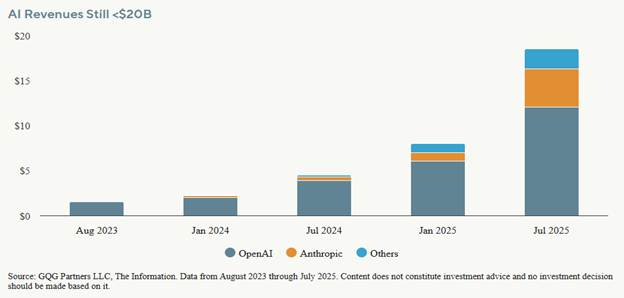

So, the current valuations can make sense given the current and projected growth rates, which are supported by AI scaling laws. Even at the extremes of 10–20x revenue multiples, this is not unprecedented—many venture capitalists routinely value early-stage, high-growth tech startups at around 15x revenue. This reflects both the nascent stage of these companies and the substantial expectations for future growth. The fundamental question now circles around future growth and whether it can continue in the future. As newer AI and larger compute begin to support product innovations like agents and agentic processes that can provide real value to customers, we think it is not far-fetched to see these high revenue growth rates continue over the next few years. Note that in the above chart of AI revenue for the frontier models, the revenues are still below $20B, but the revenue has doubled every 6 months for the past year and a half.

This is not to say that the current environment is without risks. Valuations do matter, and if the current high rates of revenue growth stall or innovation gets bogged down, we could see a period of multiple contractions across the AI industry. The companies not only need to keep innovating, but also to monetize those innovations to increase the return on investment for these large infrastructure projects. As in any innovation cycle, pockets of excess will build and potentially burst as the technology leaves a wake of disruption. As of today, we believe we are in the early stages of this build-out and monetization and have our eyes focused on the potential impact three to five years in the future. It is often said that humans tend to overestimate in the short-term and under-estimate in the long-term – and we think this is an apt description of the current sentiment around many AI companies.

Yet if we have learned one thing from the history of invention and discovery, it is that, in the long run – and often in the short one – the most daring prophecies seem laughably conservative.”

– Arthur Clarke, The Exploration of Space (1951)

As we’ve highlighted in prior newsletters, the balance we are trying to strike is to maintain appropriate and prudent diversification at a time of heightened risks across a wide range of axes. Asset allocation remains essential for weathering near-term volatility. Whether fixed income portfolios represent a certain number of future years of spending or simply an allocation for risk-management purposes, we are actively reviewing asset allocations to ensure they remain appropriately constructed.